We surveyed over 500 retirees and near-retirees to identify their top concerns, including guaranteed income, low fees, and service quality. We also interviewed licensed annuity agents nationwide to learn which companies are the most reliable and easiest to work with. Finally, we evaluated each provider using hard data, including annuity company ratings, total premiums sold and more. Every company was scored across these three dimensions to produce a well-rounded, trustworthy ranking.

- New York Life — Best for Financial Strength & Longevity

New York Life is the gold standard for retirees who prioritize safety and guaranteed lifetime income above all else. - Allianz — Best for Growth-Oriented Index Strategies

With a market-leading lineup of fixed index annuities, Allianz is ideal for buyers who want downside protection with meaningful upside participation through innovative crediting strategies. - Nationwide — Best for Flexible Income Riders

Nationwide offers one of the broadest annuity product ranges in the industry, paired with competitive lifetime income riders featuring bonus credits of up to 30%. - Lincoln Financial Group — Best for Retirement Income Planning

Lincoln Financial holds an A+ AM Best rating and stands out for its robust suite of income-focused annuities and comprehensive advisor tools, making it a strong choice for retirees building a guaranteed paycheck. - MassMutual — Best for Conservative, Safety-First Investors

One of only a handful of A++-rated annuity carriers by AM Best, MassMutual’s mutual ownership structure means profits flow back to policyholders—perfect for conservative savers who value stability over yield.

Below, you’ll find detailed profiles for the top 5 companies to help you compare what matters most.

New York Life: Most Trusted by Consumers

New York Life

Key Company Metrics

AM Best Rating: A++ (Superior)

Years in Business: 180 years

Direct Premiums Sold: $21.3 Billion

Product Availability: Fixed, Indexed, Immediate

“Their immediate and deferred income annuities are among the strongest in the market in terms of payout and stability.”

New York Life’s Strengths

| Financial Stability | ⭐⭐⭐⭐⭐ |

| Product Availability | ⭐⭐⭐⭐☆ |

| Customer Trust | ⭐⭐⭐⭐⭐ |

| Ease of Working with Agents | ⭐⭐⭐⭐☆ |

| Legacy & Lifetime Income | ⭐⭐⭐⭐⭐ |

Consumer Poll Insights

Consumers consistently rank New York Life high for lifetime income guarantees, company longevity, and confidence in claims-paying ability.

- 73% prioritize financial strength when selecting a provider

- 65% say product transparency and clear payout terms are vital

Allianz: Top Growth Protection Balance

Allianz

Key Company Metrics

AM Best Rating: A+ (Superior)

Years in Business: 129 years

Direct Premiums Sold: $23.1 Billion

Product Availability: Fixed, Indexed, Immediate

“Allianz offers some of the most innovative indexed annuities in the industry — strong cap rates, flexible riders, and consistent performance.”

Allianz’s Strengths

| Financial Stability | ⭐⭐⭐⭐☆ |

| Product Availability | ⭐⭐⭐⭐☆ |

| Customer Trust | ⭐⭐⭐⭐☆ |

| Ease of Working with Agents | ⭐⭐⭐⭐☆ |

| Innovation & Digital Tools | ⭐⭐⭐⭐⭐ |

Consumer Poll Insights

Allianz stands out for its indexed annuities, which balance growth potential with downside protection — a favorite among long-term planners.

- 70% of consumers value companies that offer customizable annuity options

- 64% prioritize online account access and modern digital tools

Nationwide: Top Annuity Variety

Nationwide

Key Company Metrics

AM Best Rating: A+ (Superior)

Years in Business: 99 years

Direct Premiums Sold: $12.85 Billion

Product Availability: Fixed, Indexed, Variable, Immediate

“Nationwide is incredibly consistent — applications are easy, and support is top-notch.”

Nationwide’s Strengths

| Financial Stability | ⭐⭐⭐⭐☆ |

| Product Availability | ⭐⭐⭐⭐⭐ |

| Customer Trust | ⭐⭐⭐⭐☆ |

| Ease of Working with Agents | ⭐⭐⭐⭐☆ |

| Flexibility & Innovation | ⭐⭐⭐⭐☆ |

Consumer Poll Insights

Nationwide is often chosen for its broad selection of products, including variable annuities with flexible income riders and robust customization options.

- 69% of consumers want companies with a wide range of annuity types

- 61% are concerned about fees and long-term flexibility

Lincoln Financial: Best for Retirement Income

Lincoln Financial Group

Key Company Metrics

AM Best Rating: A (Excellent)

Years in Business: 120 years

Direct Premiums Sold: $27.1 Billion

Product Availability: Fixed, Indexed, Variable, Immediate, Deferred Income

“They’ve built a legacy of trust and perform well with high-net-worth clients seeking estate planning solutions.”

Lincoln Financial’s Strengths

| Financial Stability | ⭐⭐⭐⭐☆ |

| Product Availability | ⭐⭐⭐⭐⭐ |

| Customer Trust | ⭐⭐⭐⭐☆ |

| Ease of Working with Agents | ⭐⭐⭐⭐☆ |

| Retirement Income Planning | ⭐⭐⭐⭐⭐ |

Consumer Poll Insights

Lincoln is widely appreciated for income-focused annuities that provide long-term security, including options with inflation protection and death benefit riders.

- 68% say guaranteed lifetime income is a top priority

- 62% care about the company’s reputation for customer service

MassMutual: Top Long-Term Stability

MassMutual

Key Company Metrics

AM Best Rating: A++ (Superior)

Years in Business: 174 years

Direct Premiums Sold: $9.09 Billion

Product Availability: Fixed, Indexed, Variable, Immediate

“MassMutual’s fixed annuities are among the most stable — ideal for clients who don’t want surprises.”

MassMutual’s Strengths

| Financial Stability | ⭐⭐⭐⭐⭐ |

| Product Availability | ⭐⭐⭐⭐☆ |

| Customer Trust | ⭐⭐⭐⭐⭐ |

| Ease of Working with Agents | ⭐⭐⭐⭐☆ |

| Conservative Planning Fit | ⭐⭐⭐⭐⭐ |

Consumer Poll Insights

MassMutual is recognized for exceptional financial strength, making it a preferred choice for conservative retirees seeking safety and predictability.

- 71% of consumers trust companies with a long-standing track record

- 67% value financial strength ratings as a top priority

Best Annuity Company Ranking Methodology

Each company’s score from the three sources was normalized and weighted as follows:

- Measurable Metrics: 50% — AM Best financial strength rating, years in business, direct premiums sold, product variety, availability across states, NAIC complaint index & J.D. Power rankings and digital tools and online access.

- Consumer Survey: 25% — We surveyed over 600 retirees and near-retirees through an independent panel. Respondents ranked what mattered most to them when selecting an annuity provider.

- Agent Poll: 25% — We also gathered qualitative input from licensed annuity agents who actively write business with multiple carriers across the U.S. These experienced professionals ranked companies based on easy of doing business, product quality and flexibility, reputation and claims-paying ability and customer experience from the advisor’s point of view.

We then assigned each company a composite score and ranked the top performers. The final list reflects a balance of trustworthiness, product strength, service quality, and real-world experience — not just financial size or advertising dollars. More about our rankings can be found on our annuity rankings methodology page.

How to Compare Annuity Companies

We selected the top annuity companies based on what matters most to real buyers: financial strength, customer satisfaction, product flexibility, and advisor insights. However, while these rankings provide a strong starting point, the best company for you will ultimately depend on your unique goals, preferences, and retirement timeline.

Whether you value top-tier credit ratings, responsive support, or income guarantees, it’s important to weigh each provider against the factors that matter most to you.

The comparison chart below highlights key criteria to help you make a confident, personalized decision.

| ANNUITY COMPANY | AM BEST RATING | YEARS IN BUSINESS | PREMIUMS SOLD ($B) | PRODUCT TYPES OFFERED | BEST COMPANY FOR |

|---|---|---|---|---|---|

| New York Life | A++ | 180 | 21.3 | Fixed, Indexed, Immediate | Lifetime Income Stability |

| Allianz | A+ | 129 | 23.1 | Fixed, Indexed, Immediate | Indexed Annuities & Digital Tools |

| Nationwide | A+ | 99 | 12.8 | Fixed, Indexed, Variable, Immediate | Variable Options & Flexibility |

| Lincoln Financial Group | A | 120 | 27.1 | Fixed, Indexed, Variable, Immediate, Deferred | Income Planning & Product Diversity |

| MassMutual | A++ | 174 | 9.1 | Fixed, Indexed, Variable, Immediate | Financial Strength & Stability |

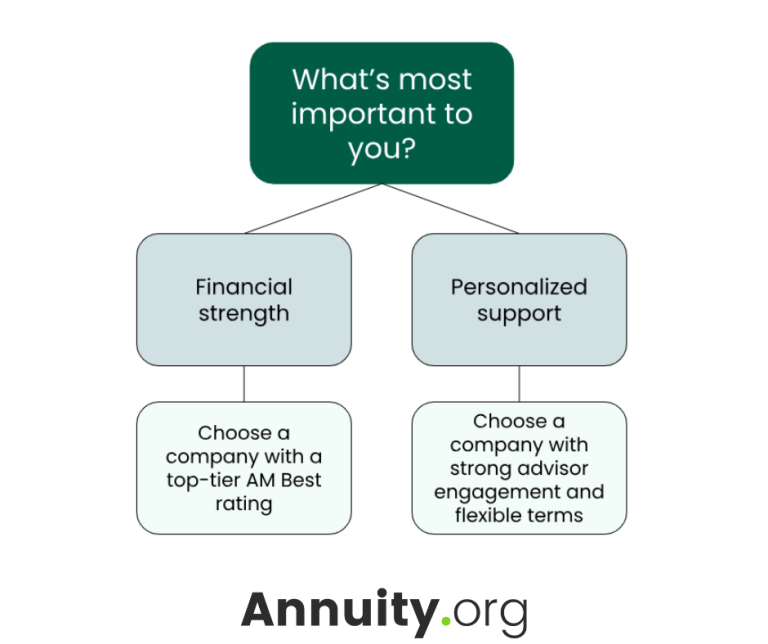

Why the “Best” Company Isn’t the Same for Everyone

When it comes to choosing an annuity provider, there’s no one-size-fits-all answer. What works best for one person might not be the right fit for another, and that’s okay. Your financial priorities, comfort level with risk, need for flexibility, and desire for support all play a role in the decision.

Some people feel most confident choosing a provider with top-tier financial ratings. Others want hands-on guidance and flexible product features. Choosing the right annuity provider starts with knowing what matters most to you.

The following real-world scenarios show how different buyers made choices based on what mattered most to them, from long-term security to hands-on service and flexible income options. Use these examples to see how your own goals might align with different types of providers.

Choosing Based on Financial Strength and Service

Linda, a 63-year-old recently retired nurse, is looking for a fixed indexed annuity to secure lifetime income while keeping pace with inflation. She’s comparing two companies: Company A, a national brand with top-rated customer service and an A- AM Best rating, and Company B, a lesser-known insurer with an A++ rating but fewer online resources and less personalized support.

Linda is concerned about market volatility and wants to ensure her money is safe for the long haul. After speaking with her advisor, she decides on Company B because of its stronger financial strength rating and longer history in the annuity market. Even though Company A offered a slightly more user-friendly experience, Linda values long-term security and the confidence that her income stream is backed by a highly rated company with deep reserves.

Her decision reflects what many annuity buyers prioritize: financial stability over convenience, especially when retirement income is on the line.

Choosing Based on Personalized Support and Flexibility

David, a 58-year-old marketing consultant planning early retirement, wants a deferred fixed annuity that allows partial withdrawals and optional riders for long-term care. He’s deciding between Company X, known for its strong financials but limited customer contact options, and Company Y, which offers slightly lower ratings but assigns each client a dedicated advisor and offers more customizable rider options.

After requesting quotes, David is impressed that Company Y’s representative takes time to walk him through different income scenarios, explains how optional inflation protection works, and follows up with personalized illustrations tailored to his goals. He also learns that Company Y allows flexible withdrawal options without early surrender charges, which aligns with his plan to possibly start a side business.

Even though Company X had a higher AM Best rating, David chooses Company Y because of its responsive service, clarity around fees, and ability to tailor the contract to his evolving needs. He feels more confident partnering with a provider that understands his specific situation and offers ongoing guidance.

This choice reflects a common real-world tradeoff: prioritizing human support and product flexibility over top-tier ratings, especially for those navigating early or nontraditional retirement paths.

Frequently Asked Questions

For immediate annuity (SPIA) payouts, the highest monthly income comes from insurers who price aggressively, often those with lower AM Best ratings. Among A-rated or better carriers, income payouts are competitive within a narrow range. Athene, MassMutual, and New York Life consistently offer strong SPIA payouts. The best way to find the highest payout is to get quotes from 3–5 carriers simultaneously through an independent broker or annuity marketplace.

Annuities are not FDIC-insured, but every state has a guaranty association that protects policyholders if an insurer becomes insolvent. Coverage is at least $250,000 in annuity benefits in all 50 states, though limits vary. In most cases, another insurer acquires the failed company’s contracts and you continue receiving payments under the new carrier. Insurance company failures are rare, but this is one reason financial strength ratings matter when choosing a provider.

Yes, and many financial advisors recommend it. Spreading your annuity purchases across multiple highly rated carriers diversifies your risk and lets you match different products to different goals. For example, a MYGA from one company for guaranteed growth alongside a SPIA from another for immediate income. This strategy also keeps each contract within your state’s guaranty association coverage limits.

Still have questions?