Key Takeaways

- The average cost of a financial advisor is about 1% of the assets they manage. The cost of a financial advisor can vary based on the type of advisor, the fee structure they use and the amount of assets they manage for you.

- Financial advisors may charge a flat fee, hourly rate or single fee for each financial project you create — such as a college savings fund or retirement plan.

- Be aware of additional fees you may have to pay for services that financial advisors offer.

What Is the Cost of Hiring a Financial Advisor?

The average cost of hiring a financial advisor is usually around 1% of the amount of assets they manage, but there is no firm rule about how much financial advisors charge. It can vary widely depending on the type of fee structure the advisor uses.

The type of advisor — from automated robo-advisors to in-person advice — can also make a big difference. Still, other financial advisors may charge flat fees, hourly rates or by each savings plan you have.

It can also vary depending on the amount of assets you have under management — 1.2% for $50,000 down to 0.59% for $30 million on average, according to U.S. News and World Report. But the range can vary from 0.25% for really large amounts of assets up to 3% for small assets.

With just $100,000 in assets under management, you’d pay $1,000 a year at that 1% average. That may sound like a lot at first, but it may be worth it if the professional guidance grows your savings faster than you can on your own.

Both the amount and manner in which you pay an advisor can vary greatly depending on the type of advisor you hire and the service they provide.

Fee Structures

Different types of financial advisors will have different types of fee structure. A fee structure is the way in which the advisor calculates the amount you will pay for their services.

There are four main types of financial advisor fee structures to be aware of — assets under management (AUM), retainers or annual flat fees, hourly fees and per-plan fees.

Financial Advisor Fees

| TYPE OF FEE | COST RANGE |

|---|---|

| Assets under management | 0.25% (robo-advisors) to 2% (in-person advisor) per year |

| Flat fees (annual retainer) | $1,000 to $7,500 per year |

| Per-plan fees | $1,000 to $3,000 per year |

| Hourly fees | $150 to $400 per hour |

Is a Financial Advisor Worth It?

Many people find that working with a financial advisor is worth it because it helps them get closer to their goals, such as planning and saving for retirement.

The 2024 Planning and Progress Study from Northwestern Mutual found that individuals who worked with a financial advisor expected to retire two years sooner than those who didn’t have an advisor. Respondents who worked with an advisor also had twice as much saved for retirement – $132,000 on average compared to $62,000 saved by those without an advisor.

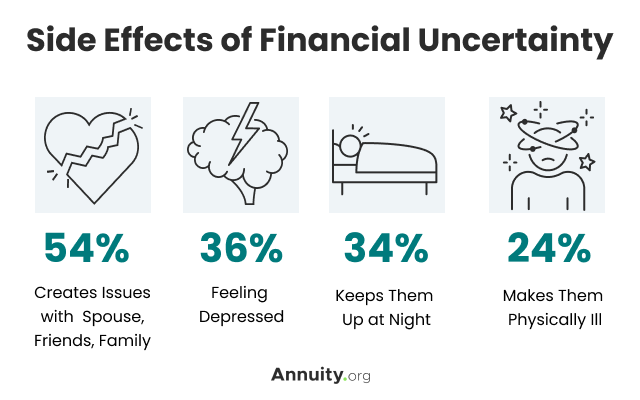

The price of avoiding professional advice could be far more than the cost of hiring a financial advisor. The study found that people reported social, mental and physical health concerns, which they blamed on their financial uncertainty.

Side Effects of Financial Uncertainty

- Creates Issues with Spouse, Friends, Family — 54%

- Feeling Depressed — 36%

- Keeps Them Up at Night — 34%

- Makes Them Physically Ill — 24%

Source: Planning & Progress Study

At the same time, you should carefully assess all fees a financial advisor charges and know about total costs involved before hiring a financial advisor.

Let’s Talk About Your Financial Goals.

Typical Financial Advisor Fees

Advisor fees are not the only way financial advisors and their firms make money. You should ask about other fees and costs that can raise the price of your financial advice.

- Commission

- Commission fees may be listed in your contract as “expenses” or “loads.” A registered representative — or RR — only receives a commission for the sale of products they recommend. You pay for the RR’s advice through the cost of the product or through high penalties for exiting the product early.

- Fee-Only

- Registered investment advisors — or RIAs — can only charge fees for their advice. Typically, these are based on the assets-under-management fee structure. Their fees are only charged on an annual, quarterly or monthly schedule. A 1% fee is common.

- Flat, Hourly or Project

- Flat and hourly fees may be similar to what an accountant or lawyer charges — a specific rate for a flat fee or for each hour spent working with you or your plan. Project fees tend to work well with a specific financial plan — say for your child’s college fund or your retirement plan.

- Hybrid or Fee-Based

- This type of fee structure combines both the assets-under-management and the commission models. You should make sure that any advisor using this method clearly explains how much each will cost you and that you understand the costs up front. Different recommendations may use one or the other, so make sure you know which applies each time you seek advice going forward.

- Investment Fees

- In addition to your payment to the financial advisor, you may be paying an investment fee — also called an expense ratio. In addition to paying the advisor, you may have to pay a fee to the investment product provider. This can easily double your out-of-pocket costs so be sure to ask exactly what your total payments will be. It will be spelled out in your account’s contract.

- Wrapped Fees

- These can be hidden fees. They are common with employer-based retirement plans such as 401(k) plans. They work similarly to commissions — with the advisor receiving payment from a company. If you don’t write a check to the advisor, then someone else is paying them. You should ask who it is and how the arrangement works.

Other Common Fees with Financial Advisors

It’s also important to check your invoices to make sure there are no inaccuracies or changes to the fees you are paying. If an advisor changes their fee structure or renegotiates fees, it can lead to errors in your invoice.

How Costs Differ by Advisor Type

What you pay and what you get in return depends largely on the type of financial advisor you choose.

Online and robo-advisors automate a lot of the portfolio-building and management process. But they can provide you with tools and guidance. Online financial advisors can even provide a human element with professional and Certified Financial Planners™ providing additional or even customized advice.

Traditional advisors can provide different levels of services — often defined by their fee structure.

Robo-Advisors

Robo-advisors typically charge the lowest fees, but they don’t necessarily provide the highly personalized service that you get with an in-person advisor.

These are online services that help you select and manage investments. Robo-advisors ask questions about your financial goals, the time frame to achieve them and your risk tolerance. Then, they build and manage your investments based on that information.

Robo-advisors charge on an assets-under-management basis. If you have $100,000 in assets, expect to pay $250 to $500 a year for their service.

Online Financial Planning Services

Similar to robo-advisors, online financial planning services provide more offerings, like what you’d expect from traditional financial advisors. But instead of meeting with an advisor in-person, online services handle your plan online, over the phone or in video meetings.

Online financial planning services provide access to financial professionals who can help you shape a wide-ranging financial plan. Many offer access to a Certified Financial Planner™ — CFP™ — a credentialed financial professional with specialized training.

The assets-under-management cost for online financial planning services is slightly higher than robo-advisors, but still below hiring an in-person advisor. Some services charge flat annual fees, typically starting at $1,000 and can easily be higher.

Traditional Advisors

Traditional, in-person financial advisors use wide ranging fee structures and are the most expensive option. But you get personalized advice, guidance and planning services customized to your specific goal.

Those who charge an assets-under-management fee typically charge around the 1% average — but may set a minimum amount of assets before taking you on as a client. This can be $250,000 or more.

Traditional advisors who charge a retainer or flat annual fee typically will take on just about any amount of assets you have. But their annual fee — often between $1,000 and $7,500 — tends to be higher the more complex your portfolio becomes.

The U.S. Securities and Exchange Commission has an online Advisor Public Disclosure website you can use to check the background and experience of any financial advisor you are considering.

Those who charge an hourly fee — as much as $400 per hour — usually charge the same rate to anyone, regardless of the amount of assets. You simply pay for their time. These advisors will typically set up your plan, but you manage it — there is no ongoing guidance unless you pay for the time.

Traditional advisors who charge a flat fee may offer the least services. Typically, they’ll charge you a one-time fee to set up a plan, but you are responsible for its management from that point forward. Some flat fee planners also provide ongoing services where that flat fee is an annual payment.

Alternatives to Hiring a Financial Advisor

You may not need a financial advisor just to file your taxes or if your savings are primarily through your employer’s retirement plan or an IRA.

If you want to handle your own financial planning, you will need to learn as much as you can about your options to save, invest and build your wealth.

- Choose a different type of financial professional.

- If you primarily need tax advice or preparation, consider a CPA. An enrolled agent may be a less expensive option. These professionals may also offer limited planning services.

- Read about and study personal finance.

- While you won’t learn as much as a certified financial advisor who has years of training and education on top of experience, reading about personal finance can make yourself more knowledgeable about the aspects of your finances that matter specifically to you.

- Consider index funds.

- Index funds base their returns on the performance of market indexes — such as the S&P 500. Your return on investment in these funds mirrors the performance of the index. These allow you to easily diversify.

- Consider a low-cost brokerage.

- Schwab or Fidelity are among a wide variety of low-cost brokerage firms that allow you to purchase wide-ranging investment options for relatively low fees.

Financial Advisor Alternatives

But if you have your own business, a wide range of investments, want to build your investment portfolio or come into a sudden windfall — such as an inheritance or lottery jackpot — you may want to consider having the professional expertise that a financial advisor can provide to grow your wealth.