What Is a 401(k) Plan?

A 401(k) is a type of defined contribution retirement plan available to employees of for-profit enterprises extending these retirement options. With a 401(k) plan, participants willingly set aside a portion of their earnings into an individual retirement savings account, staying within the annual limits set by the Internal Revenue Service (IRS).

Key Facts About 401(K) Plans

- The 2025 401(k) contribution limits are $23,500 if you’re younger than 50, $31,000 if you’re at least 50 and $34,750 if you’re 60 to 63.

- A 401(k) isn’t an investment itself; it’s an account with money that plan participants can use to select investments available through their employers.

- While 401(k)s offer benefits like high contribution limits, federal protection and potential free money, they can come with fees, tax penalties and limited options.

- Withdrawals from traditional 401(k)s are taxed as ordinary income, while Roth 401(k) distributions aren’t taxed if a participant is at least age 59 ½ and the account is open for at least five years.

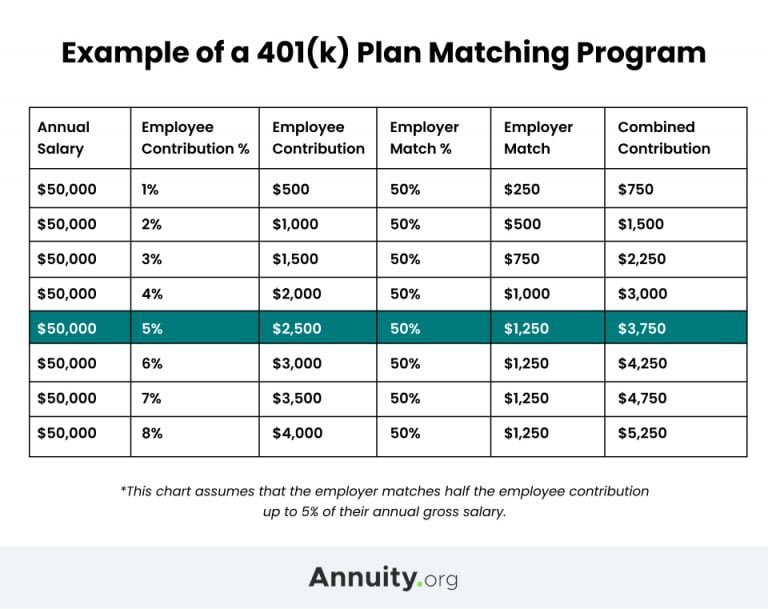

For example, if you earn $50,000 annually and contribute 5% of your income, savings for the year would be $2,500 divided among the number of paychecks you receive.

By leveraging traditional 401(k) contributions, individuals can lower their federal income tax burden, as these contributions are deducted from taxable earnings. State tax implications may differ. Notably, both contributions and earnings remain untaxed until withdrawals are made. Many employers also match their employees’ contributions.

401(k) Contribution Limit

In 2025, the 401(k) contribution ceiling stands at $23,500 with additional catch-up limits based on age. Participants aged 50 and older can contribute an extra $7,500 ($31,000 annually). Those who are 60 to 63 can contribute an extra $11,250 ($34,750 annually).

It’s important to note that these maximum contribution limits undergo annual indexing to account for inflation.

401(k) Features

While not inherently an investment, a 401(k) functions as an account where plan participants choose investments provided by sponsoring employers. Employers, generally through plan providers, curate a list of investment choices for participants to choose from. Choices will often include mutual funds and exchange traded funds (ETFs), such as stocks and bonds.

Most commonly, the plan administrator invests the 401(k) contributions into a target date fund. Target date funds are made up of different asset holdings and are designed to start more aggressively invested and become more conservative as the investor approaches retirement. Asset managers tweak the allocations within a target date fund over the years, increasing bond and cash holdings while decreasing the investment in stocks.

Some target date funds now allocate part of the fund’s cash holdings towards an annuity, so the fund holder can work towards generating a lifetime income stream while saving for retirement.

It is also possible to rollover 401(k) funds into another qualifying account, such as a traditional IRA, for a broader selection of investments, or an annuity, for a guaranteed stream of lifetime income. With a direct rollover, investment earnings continue to grow tax-deferred.

Types of 401(k) Plans

A comparison chart from the Internal Revenue Service (IRS) describes differences in plan contributions, income limits and distributions. Employers generally offer two categories of 401(k) plans for their employees: traditional and Roth.

Traditional 401(k) Plans

Traditional 401(k) plans allow employees to contribute pre-tax dollars that are invested according to their selected asset allocation. Withdrawals from traditional 401(k) plans are typically taxed as ordinary income.

Roth 401(k) Plans

Roth 401(k) plans operate on after-tax contributions. Distributions from Roth 401(k) plans are not taxed so long as they meet the criteria for qualified distributions. The account must be held for at least five years, and the participant must be at least 59 ½ years old. Distributions resulting from disability or death also meet the criteria.

Since 2024, because of the SECURE 2.0 Act, Roth 401(k) distributions are no longer required, which means accounts can continue to grow intact. Heirs who inherit Roth 401(k)s also receive tax-free money and must empty the account within 10 years. Inherited account rules are complex, and it is advisable to seek professional advice as needed.

In order to get the most benefit from your 401k plan, it’s important to know how it functions. While most participants know the contribution limits, many fail to understand distribution rules. These are particularly important because failing to follow them can result in unnecessary taxes and penalties. Another simple but significant misunderstanding that I’ve seen more than once is that a 401k is an account, not an investment. After you contribute money you still need to make specific investment selections to ensure your money is working for you.

Brandon Renfro, Ph.D., CFP®, RICP®, EACo-Owner of Belonging Wealth ManagementAs a Certified Financial Planner™ professional and Retired Income Certified Professional®, Brandon Renfro is well-versed in the financial information and strategies needed to meet retirement goals. In addition to co-owning Belonging Wealth Management and assisting clients, Brandon writes regularly for financial publications.

How Does a 401(k) Plan Work?

401(k) plans are designed to help employees grow their retirement savings. Once a plan is established, it goes through a period of tax-deferred growth before an employee reaches retirement. Decades of tax-deferred compounded interest can result in significant wealth accumulation.

A 401(k) plan’s lifespan can be summarized in four steps:

- Step 1

- Employers offer a 401(k) plan in their benefits package. Some workers are automatically enrolled with a default contribution amount and an array of investments. Otherwise, you can enroll yourself and select specific investments from the plan’s various options. Key factors to consider are your investment knowledge, time horizon and risk tolerance.

- Step 2

- You contribute pre-tax money from your paycheck directly into a traditional 401(k). Your employer may match all or part of your contribution. Employer matches are the equivalent of receiving a 50% to 100% return on your money. Some employers also offer Roth 401(k)s, where you contribute money after taxes have been taken out.

- Step 3

- Contributions to the plan are invested in the selections you’ve made, and earnings fluctuate based on the performance of these investments over time. In a traditional account, both plan contributions and earnings experience tax-deferred growth until the point of withdrawal, usually during retirement. After reaching age 59 ½, you may begin withdrawing funds without a 10% early withdrawal penalty.

- Step 4

- Withdrawals from a 401(k) are taxed as ordinary income, irrespective of age. Depending on your birth year, RMDs must begin either at age 73 (for those born between 1951 and 1959) or at age 75 (for those born in 1960 or later). Older retirees initiate RMDs either at age 70 ½ or 72. The period between age 59 ½ and the RMD start date is considered “financial gap years,” during which withdrawals are optional, offering flexibility for retirees during this transitional period.

401(k) Lifespan

Read More: How To Find a Lost 401(k)

Pros and Cons of 401(k) Plans

401(k) plans have advantages and disadvantages. Understanding these pros and cons can help you with your financial decision-making.

- Federal Protection Under ERISA

- The Employee Retirement Income Security Act of 1974 (ERISA) is a federal law that protects retirement savings accounts by setting standards for employers. This is a good thing and helps ensure adequate plan funding. Some other employer plans, like 403(b) plans, may lack ERISA protection.

- Employer Matching

- Employers can, but are not required to, match employee contributions, essentially adding “free money.” For example, if you contribute 10% of your income, they may match the full 10% or to a certain percentage, such as 4% or 6%. Employers may have specific rules, such as delaying matching until an employee is vested in the company or has been employed for a certain period of time.

- High Contribution Limits

- 401(k) plan,0 contribution limits are much higher than those for individual retirement accounts (IRAs). In 2025, the limits are $23,500 ($31,000 for ages 50 and older and $34,750 for ages 60 to 63) for 401(k)s compared to $7,000 ($8,000 for ages 50 and older) for IRAs.

Pros of 401(k) Plans

While there are strong advantages to a 401(k) plan, it’s important to be aware of the disadvantages before deciding to open an account.

- Limited Investment Options

- 401(k) plans typically offer a limited selection of investment options compared to, for example, IRAs held in a brokerage account. Investors who prefer a wide range of choices may consider this a drawback.

- Early Withdrawal Penalties

- If you find yourself needing to make a withdrawal from a 401(k) plan before reaching the age of 59 ½, be aware that a 10% penalty is typically applied. Additionally, surpassing the annual limit, set at $23,500 in 2025 with adjustments for the cost of living, results in a 6% penalty. To circumvent these penalties, one alternative is to consider borrowing from your 401(k) instead of making a direct withdrawal. It’s crucial to ensure strict adherence to the established rules governing 401(k) plans to avoid any unintended consequences.

- Account Expenses

- Investments within a 401(k) account typically incur maintenance fees or expenses, which can impede overall investment performance. The extent of these costs varies, with low-cost index funds or ETFs generally having lower expense ratios compared to actively managed mutual funds.

Cons of 401(k) Plans

It is important to understand 401(k) rules and how they differ from the rules of other retirement savings plans. To maximize the benefits of your plan and avoid unnecessary penalties, read all documents about your 401(k) and contact your company HR office or a financial advisor with any questions you may have.

Financial advisors can also help you grow multiple streams of tax-diversified retirement income. You may benefit from putting extra funds into a Roth or traditional IRA, taxable investment account or annuity to insure against longevity risk.

What If the Market Drops the Year You Retire?

Tax Treatment of 401(k)Plans

401(k) plans affect income taxes before and after retirement. The amount of tax you owe depends on the type of plan. Traditional 401(k) plan contributions are tax-deferred and excluded from taxable income when made; however, withdrawals are subject to income tax. Qualified distributions from Roth 401(k) plans are not taxed because taxes were already paid on the money before contributing to the plan.

Traditional or Roth 401(k)

A key factor in deciding which 401(k) type to choose is what you think your future tax rate will be compared to your current tax rate. Individuals who expect their tax rate to drop in retirement often select a traditional 401(k), while those who expect their tax rate to rise often choose a Roth IRA.

A Hybrid Approach

The above advice is sound; however, many people have no idea what their income and wealth will be decades in the future, or what federal tax rates will be. Another approach is to “hedge your bets” and spread 401(k) savings between traditional and Roth accounts.

Professor David Brown at the University of Arizona recommends adding 20 to your age for the percentage of savings in a traditional account, with the remainder going into a Roth account.

For instance, if you’re 30, the recommended split is half and half between Roth and traditional accounts, calculated by adding 20 to your age (30 + 20 = 50).