In terms of investing, risk tolerance refers to the amount of risk a person is willing to assume within their investment portfolio. It is largely dependent on an individual’s investing time horizon.

Generally, the longer your investing horizon, the higher your risk tolerance. Conversely, the shorter your horizon, the lower your risk tolerance. That said, there are various factors that influence risk tolerance.

The Two Components of Risk Tolerance

Risk tolerance consists of one’s willingness and capacity to assume risk, particularly when it comes to making financial investments. Willingness refers to your psychological leanings regarding uncertainty (risk-seeker vs. risk-avoider). Capacity refers to your level of financial wellness and ability to endure losses.

While the two components of risk tolerance are usually aligned, they can diverge. When that happens, an investor should refrain from allowing a psychological inclination to overshadow their capacity. Doing so will likely lead to better financial outcomes.

It’s important not to assume that you just have one risk tolerance. Take two different accounts with long (10+ year) time horizons – a college fund for a young child and a retirement account. I have had past clients who have had vastly different risk tolerances for those two accounts (aggressive in the retirement account and moderately conservative in the college fund). So not only does each person have their own risk tolerance, each account may have it’s own too.

Chip StapletonFINRA Series 7 and Series 66 License HolderChip Stapleton is a financial advisor who has spent the past several years of his career working primarily in financial planning and wealth management. He is a FINRA Series 7 and Series 66 license holder and passed the CFA Level II exam in 2022.

Factors That Influence Risk Tolerance

As indicated previously, investing time horizon significantly influences risk tolerance. Below, we expand on the importance of this factor and discuss a few other prominent criteria that determine risk tolerance.

Investing Time Horizon

Investing time horizon is the amount of time you have to achieve a financial goal, such as making a down payment on a home, funding a child’s college education or financing your retirement.

Generally, the longer the horizon, the greater your ability to withstand market fluctuations and temporary losses. a relatively long horizon, you can usually invest aggressively – with an eye toward long-term wealth accumulation, not short-term market volatility.

On the other hand, with a relatively short horizon, you do not have the ability to withstand significant market declines. In this situation, investment stability and liquidity is much more important than potential growth.

Investment Objectives

Investment objectives are the goals you intend to accomplish through your investment positions. Generally, they include some combination of ensuring liquidity, preserving capital, generating income and fueling growth.

Collectively, these objectives help determine your level of risk tolerance and the types of investment strategies you should pursue.

For example, if you have many years until retirement and are predominantly focused on accumulating wealth, you are likely to be highly tolerant of risk and well-positioned to invest in growth-oriented assets.

Alternatively, if you are retired and only care about safely generating cash flows to meet your spending needs, you are likely to be very intolerant of risk and well-positioned to own stable-value, income-bearing instruments.

Comfort With Volatility

Beyond your time horizon and investment objectives, risk tolerance depends on your psychological response to market volatility. You may have the financial ability to endure turbulent markets, but extreme drawdowns could be mentally overwhelming. Or, your finances may be deficient, but you may have little to no concern for market volatility.

This brings us back to a key idea expressed above. Risk tolerance has two components – willingness and capacity – and they need to be married to establish a holistic tolerance for risk. Finding a balance can be challenging, but it’s important for your financial stability.

Levels of Risk Tolerance

The most discernible sign of your risk tolerance level is the strategic design (or asset allocation) of your investment portfolio. There are three fundamental asset allocation structures.

- Conservative

- A conservative portfolio is appropriate for investors that have high income and liquidity needs, and minimal ability to withstand market volatility and sharp drawdowns. For them, capital preservation is a high priority. Oftentimes, a conservative asset allocation is suitable for investors that are near or in retirement.

- Aggressive

- An aggressive portfolio is appropriate for investors that have minimal liquidity needs and value long-term growth over income and stability. Generally, an aggressive asset allocation is best for relatively young investors that can leave their money invested over multiple economic cycles, and have time to weather market downturns.

- Moderate

- A moderate portfolio lies between the conservative and aggressive asset allocation structures. It is best for investors that desire a balanced mix of assets that offer liquidity, safety, income and growth potential. This “middle of the road” structure is popular with many investors and can be shifted to favor either end of the risk tolerance spectrum.

3 Fundamental Asset Allocation Structures

It’s also important to know that risk tolerance can fluctuate over time depending on your financial needs and life circumstances. Generally, it declines as you get closer to retirement, and it levels out during your nonworking years.

Determining and Articulating Risk Tolerance

Assessing risk tolerance can be difficult to do, which is why many investors leverage the help of financial advisors. Reputable advisors assess risk tolerance by asking clients a series of questions that sheds light on their financial condition, investing objectives and time horizon, psychological leanings and behavioral biases.

The CFA Institute underscores this assertion, pointing out that best practice is “to use psychometric tools (often questionnaires) that have demonstrated reliability and validity in predicting an investor’s emotional and behavioral tendencies around loss of portfolio value and investing discipline.”

Here are some questions that you should ask yourself to assess your level of risk tolerance, according to the Financial Industry Regulatory Authority (FINRA).

Examples of Risk Tolerance Questions

- What are your objectives for the account?

- What is your investment time horizon?

- Are you counting on this money to provide you with essential funds, either now or in the future?

- What are your short- and long-term spending requirements?

- Are you generally a cautious person, or more of a risk-taker?

Assess your risk tolerance by using the investment risk tolerance calculator.

How Does Risk Tolerance Influence an Investment Portfolio?

Risk tolerance has a significant impact on investment portfolios. In general, investors with high levels of risk tolerance usually have very large allocations of growth-oriented assets, such as stocks and variable annuities, in their portfolios.

Conversely, investors with low levels of risk tolerance usually maintain large allocations of stable-value, income-oriented assets, such as investment-grade bonds and fixed and indexed annuities.

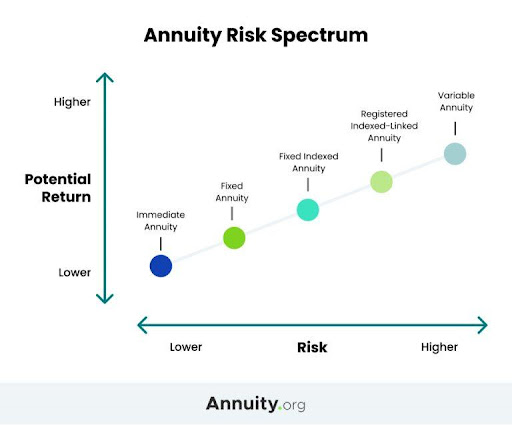

A Closer Look at Annuities

An annuity is a financial contract issued by an insurance company. Investors make a lump-sum purchase in exchange for a customizable series of immediate or deferred income distributions.

There are many annuities available, all of which can be categorized into one of the following three types of annuities.

- Can be immediate or deferred and are the safest type of annuity, offering investors a guaranteed rate of interest with zero volatility.

- Deferred in nature and a bit riskier than fixed annuities. However, they offer upside potential and downside protection.

- Can be immediate or deferred and are the riskiest type of annuity. They have investment positions in volatile assets, such as stocks and bonds, which can lose value in adverse market environments.

3 Types of Annuities

Other Frequently Asked Questions About Risk Tolerance

Investment risk is defined as the amount of risk you’re willing and able to assume when making an investment in a financial asset. You may be more risk tolerant if you want to maximize growth and have time to withstand market downturns and potential losses. Risk averse investors typically prefer stable investments with more liquidity and limited volatility.

The risk-return tradeoff is a fundamental investing concept that says higher levels of returns are only attainable by assuming higher levels of risk. The opposite is also true—reducing investment risk typically means that you’re forgoing growth potential in favor of stability.

Risk tolerance varies from one investor to the next depending on a variety of factors, including their investing horizon, investment objectives and comfort level with risk. Generally, the longer your horizon, the higher your risk tolerance and vice versa.

It’s typically recommended to reassess your risk tolerance whenever your financial condition or life circumstances change significantly, or at least every few years. If you work with a financial advisor, consult with them about the optimal cadence for your situation.