Receiving Your Casino Winnings

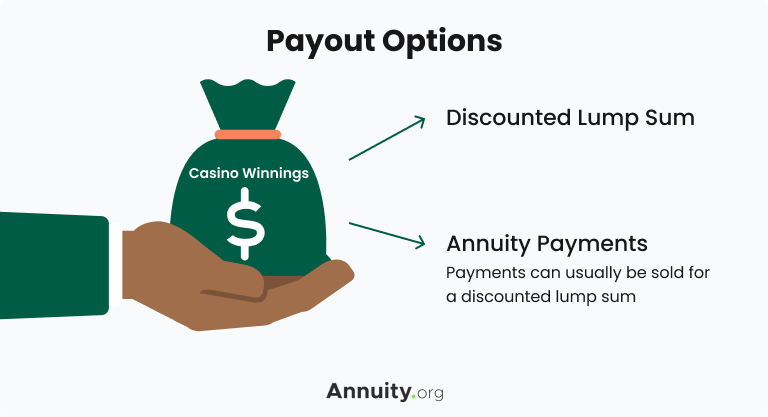

Winning big at the casino comes with tax implications and financial decisions, especially when choosing the best payout method for your financial needs. If the winnings are $25,000 or less, casinos usually limit payout options to cash or a check. If they exceed $25,000, you can typically choose between a lump sum or a stream of annuity payments.

Your payout options may change depending on the casino’s location and gambling game. Not all casinos allow you to choose how your earnings are paid out; the casino may choose for you.

While taking a single lump sum can be helpful for addressing major financial needs such as tuition fees or urgent medical bills, receiving a lump-sum payment can also negatively influence spending and saving habits by making the winnings available for immediate spending. Also, remember that lump-sum payments are subject to taxes as ordinary income, which can cut out a considerable amount of your earnings.

Key Facts About Casino Earnings:

- Casinos typically pay winnings of less than $25,000 by cash or check.

- They may disburse larger winnings either as a lump sum or as an annuity.

- Some casinos won’t allow you to choose how to receive winnings.

- Winners of large jackpots who are allowed to choose how to receive their winnings generally have up to 90 days to decide if they want a lump sum or an annuity.

Receiving casino winnings as annuity payments can help provide a controlled income stream over a longer period. These payments aren’t taxed until withdrawal, allowing the money to accumulate interest. Yet, this option restricts immediate access to a large portion of your winnings, which might pose a challenge during financial emergencies.

Winners of large jackpots typically have up to 90 days to decide if they prefer a lump sum or an annuity.

If you receive winnings in an annuity, you may still be able to sell all or a part of your annuity on the secondary market for a lump sum later. That lump sum will be less than what you would have originally received in annuity payments because secondary market buyers purchase at a discount rate.

If given a choice of payout options, it may be wise to consult with a financial advisor or tax attorney to help determine the best decision.

Need Access to Your Money Sooner?

Tax Implications of Different Payout Options

All gambling winnings — specifically those from lottery payouts, poker tournaments, horse races and slot machines — are taxable at the federal level. This means your casino earnings can place you in a higher tax bracket.

While a lump sum provides a bulk amount of cash all at once, winners must pay taxes on the entire sum within the same year it’s distributed. However, the taxes are paid only once. This option may work best for those looking to pay off debt or address other immediate financial needs.

Claiming an annuity from a casino means committing your winnings to a long-term payment plan that can take 20 to 30 years to fully payout. This guarantees an additional income stream over time — it also guarantees extended income tax liability, because you will pay taxes on those earnings for each year in which you receive them.

The IRS handles federal taxes on gambling winnings. For certain games with larger winnings, payers will furnish winners with an IRS Form W-2G.

No matter the amount, all winnings must be reported on the next tax return. A winner will generally only receive a Form W-2G if the earnings meet certain thresholds:

- $600 or more in gambling winnings (other than winnings from bingo, keno, slot machines and poker tournaments, discussed below) if the amount is at least 300 times your bet

- $2,000 or more from a slot machine or bingo game

- $1,500 or more in keno winnings

- $5,000 or more in a poker tournament

- Any winnings subject to a federal income tax withholding requirement

Source: IRS

Under specified conditions, including when winnings minus the wager exceed $5,000 and the winnings are at least 300 times the wager, the IRS requires the payer to withhold 24% of winnings before paying the final amount.

Some winnings may also be taxable at the state level. Each state has its own set of regulations for gambling taxes, so researching local requirements before filing your next tax return is important.

Lump Sum vs. Annuity Payments for Casino Winnings

Opting for a lump sum from the casino means accepting a discounted rate, usually around 50% to 60% of the total winnings. To put this into perspective, a $1.55 billion jackpot winner selecting the lump-sum option might only receive approximately $757.2 million, as reported by Kiplinger.

Consider the pros and cons of both payout methods to determine which option better suits your needs and future plans.

Pros and Cons of Taking a Lump Sum

Pros

- Immediate access to a large sum of money

- Useful for urgent financial needs

- Taxes are paid only once

Cons

- Comes at a significant discount

- Can place you in a higher tax bracket

- Can negatively influence saving and spending habits

Pros and Cons of Choosing Annuity Payments

Pros

- Provide a long-term stream of income

- Potential to avoid immediately moving to a higher tax bracket

- Generally leads to a larger overall payout

- Option to sell the remaining payments for a lump sum later if you change your mind

Cons

- Less liquidity

- Taxes are paid on each withdrawal

- Inflation can reduce the buying power of your future payments

Explore Options for Future Payments

Frequently Asked Questions About Casino Winnings & Annuity Payments

Casino winnings are fully taxable and can bump you into a higher tax bracket. How much you win determines how you’re taxed. The casino will take 24% of larger winnings for the IRS before paying you your lump sum. Taking winnings as an annuity over 20 or 30 years may reduce your tax burden and keep you in a lower tax bracket.

You are legally required to report all casino winnings to the IRS through Form 1040. If you earn above a certain threshold, you may also receive a Form W-2G. Even without this form, all winnings need to be reported.

Those seeking a consistent income stream over several years and aiming to maximize their total payout might find an annuity the more fitting option.