How an Annuity Cap Rate Works

An annuity cap rate is simply a ceiling on growth.

Your fixed index annuity is tied to a market index, such as the S&P 500. Each year, the annuity company looks at how that index performed and credits interest up to the cap rate stated in your contract.

Think of it like this:

- The index measures market movement

- The annuity credits interest

- The cap rate limits how high that interest can go

If the index does well, you participate, but only to a point. If the index does poorly, you don’t lose money due to market declines.

This structure is what allows indexed annuities to offer growth potential without direct market risk.

Annuity Cap Rate Example

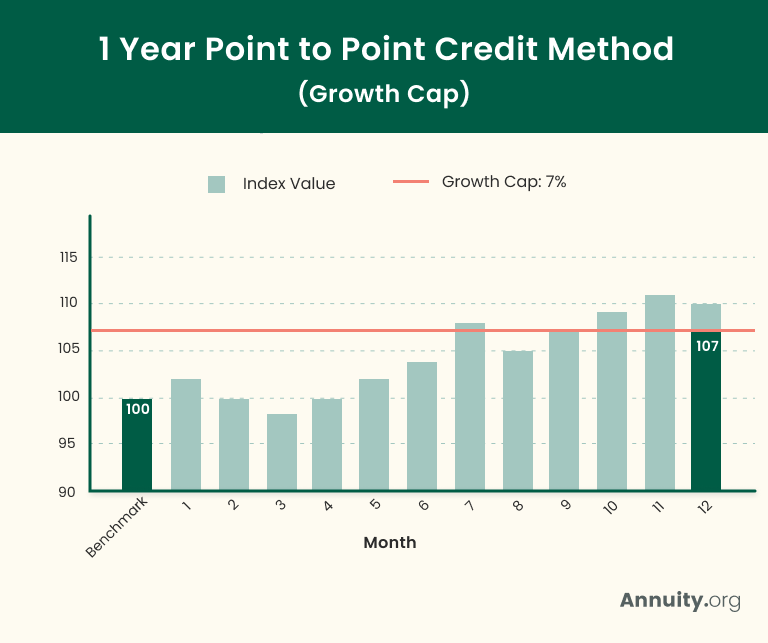

Suppose you own a fixed index annuity with a 7% cap rate and a one-year crediting period. If the linked market index gains 10%, your annuity would credit 7%, since the cap limits the amount of interest that can be applied.

If the index instead declines 12%, your credited interest is typically 0% — not a loss. Your account value remains unchanged.

For many near-retirees, this trade-off means giving up some upside in strong markets in exchange for protection during downturns.

Why Do Annuity Cap Rates Exist?

Annuity cap rates exist so insurers can limit upside gains while protecting annuity owners from market losses.

Annuity companies assume the risk of market losses. To do that sustainably, they need tools to manage how much upside they promise during strong market years. The annuity cap rate is one of those tools.

Without caps:

- Providers couldn’t guarantee principal protection

- Indexed annuities would either be riskier or unavailable

- Costs would likely show up elsewhere (fees or restrictions)

In other words, cap rates are part of the price you pay for protection.

You can think of rate caps as a type of fee or cost (though they’re not technically a fee). If you want to transfer the downside risk to the annuity company, there is a cost associated. In the case of fixed index annuities and RILAs, the cost is the cap on interest rates.

Chip StapletonFINRA Series 7 and Series 66 License HolderChip Stapleton is a financial advisor who has spent the past several years of his career working primarily in financial planning and wealth management. He is a FINRA Series 7 and Series 66 license holder and passed the CFA Level II exam in 2022.

Do Annuity Cap Rates Change Over Time?

Yes, annuity cap rates can change over time, and most indexed annuities allow providers to reset cap rates annually.

That doesn’t mean they change every year, but they can, depending on:

- Interest rate environments

- Market volatility

- The provider’s internal costs

This is why understanding today’s annuity cap rate is important — but understanding the range of possible future caps matters just as much.

A licensed annuity specialist can help you compare contracts based not just on today’s cap but on how those caps have historically adjusted.

Annuity Cap Rate vs. Other Crediting Methods

Cap rates are just one way providers limit interest crediting. Indexed annuities may use cap rates, participation rates or spreads, and knowing the difference can make it easier to compare options side by side.

Cap Rate

Sets a ceiling on how much interest your annuity can earn in a given period, even if the index performs higher.

Example: You do not see your index’s full growth of 13% due to your annuity’s annual cap of 7%.

Participation Rate

Determines the percentage of the index’s gain that’s credited to your annuity.

Example: You are only credited 9% of your index’s 10% growth due to your annuity’s participation rate of 90%.

Spread

Subtracts a set percentage from the index’s return before interest is credited.

Example: You only receive a 1% return once your 5% spread deduction is applied to your index’s 6% earnings.

Some annuities use just one of these. Others combine them. Understanding which method applies helps you compare “apples to apples” instead of relying on headline numbers.

Example: Your annuity grows by 10%, but your 90% participation rate limits your credited interest to 9%. Your contract’s annual cap further reduces this to 7%.

Understanding which method (or methods) applies helps you compare “apples to apples” instead of relying on headline numbers.

Find Out How Much Growth You Could Lock In

When an Annuity Cap Rate Matters Most

Cap rates tend to matter more if:

- Markets experience strong, sustained growth

- You’re still in the accumulation phase

- You’re comparing multiple indexed annuities side by side

They often matter less if:

- Your goal is income, not maximum growth

- You value predictability over performance chasing

- You’re using the annuity as a defensive part of a broader plan

Is an Indexed Annuity With a Cap Rate Right for You?

You might see yourself in this type of annuity if you’re thinking:

- “I don’t want another market crash to derail my retirement.”

- “I’m okay giving up some upside if I know I won’t lose principal.”

- “I want growth potential but not market stress.”

If you’re unsure, seeing how different annuity cap rates affect real outcomes (using your age, goals and timeline) can make the decision much clearer.