Investment markets remained volatile into the third quarter of 2023. Economic uncertainty, persistent inflation and rising interest rates each weigh on stock and bond prices. However, these factors also have an influence on indexed annuities, but does the structure of indexed annuities offer investors any protections?

Do Investment Risks Impact Indexed Annuities?

While anything that influences investment returns affects indexed annuities, the effects differ from those experienced with other types of annuities.

The primary purpose of owning an annuity is to enjoy an investment return during the accumulation period.

In the case of a variable annuity, that return is often linked to an underlying portfolio of mutual funds. In contrast, the return of an indexed annuity is linked to a recognized market index, such as the S&P 500.

However, there are two distinctive characteristics of indexed annuities: loss protection and guaranteed minimum returns.

Loss Protection

An indexed annuity can potentially eliminate downside exposure. For instance, if the underlying index loses 10% in a given year, the investor won’t incur any losses; the return for that year would be zero.

A different version of indexed annuities is available for investors who are willing to take on some risk. A registered index-linked annuity allows investors to specify the amount of downside exposure they are willing to assume.

Guaranteed Minimum Returns

Some indexed annuities offer investors an opportunity to earn a minimum guaranteed rate of return (typically 1% to 3%) regardless of how the underlying index performs.

For example, if the index loses 10% in a given year, the investor will still earn the minimum (1% to 3%) return. This feature is not available in registered index-linked annuities.

Investment Returns on Indexed Annuities

Indexed annuities are complex investments. The valuable benefits of loss protection and a guaranteed minimum rate of return do come with a cost.

In exchange for the features that assist investors in preserving capital in declining markets, there is a limitation on the return they can participate in when markets perform well.

Investment returns on an indexed annuity may be capped at a specific rate of return, subject to a specific percentage spread or restricted to a proportion of the index’s actual return.

Limiting an investor’s potential upside return is the trade-off for the downside protection these contracts provide.

Investment Market Highlights at Quarter End

Common stocks have experienced considerable volatility throughout 2023. After surging by nearly 20% in the first half of the year, the S&P 500 has retreated by almost 7% from its peak in July.

The S&P 500 opened on January 3rd at 3853.29, reached its highest point on July 27th at 4607.07 and closed the third quarter at 4288.05.

Despite remaining in positive territory for the year, with the S&P staying above 4100 throughout October, these gains have been accompanied by a significant amount of volatility.

On September 29, 2023, the annualized price volatility of the S&P 500 averaged nearly 16%.

In contrast, bonds performed considerably worse than stocks during the first nine months of 2023. Long-term treasury bonds lost over 16% of their value since the beginning of the year, with the majority of this decline occurring in the last six months.

The decline in bond prices can be attributed to the rising interest rates. Rates have increased at both the long and short ends of the yield curve. The federal funds rate has risen by 23% since the start of 2023.

At the end of January, the rate stood at 4.3%, and it had climbed to over 5.3% by the end of the third quarter.

While higher interest rates have been linked to declines in both stock and bond prices, they have also had an impact in curbing inflation. The increase in short-term rates is a result of intentional monetary tightening policy.

Rising Inflation Prompted Interest Rate Increases

Inflation had been rising since March 2021 when the Fed Funds rate was at 0.07%. It continued to creep higher incrementally until the Federal Reserve began raising interest rates in early 2022. By May 2022, inflation had reached its highest point in 40 years.

However, Fed tightening remained restrained. When inflation peaked at 9.1% in June 2022, the Fed Funds rate was just 1.21%. There have been 11 increases in the Fed Funds rate since the tightening began, which seems to be having an impact. Consumer price inflation (CPI) for September rose by 0.4%, marking a 3.7% increase over the previous year.

Putting Inflation, Interest Rates and Volatility Into Perspective

Consumers who miss announcements made by the Federal Reserve about inflation know that it remains higher than they would like. Nevertheless, Fed tightening has caused it to ease.

The increase in the cost of borrowing and higher interest rates have a negative effect on bond prices, contributing to overall stock market volatility.

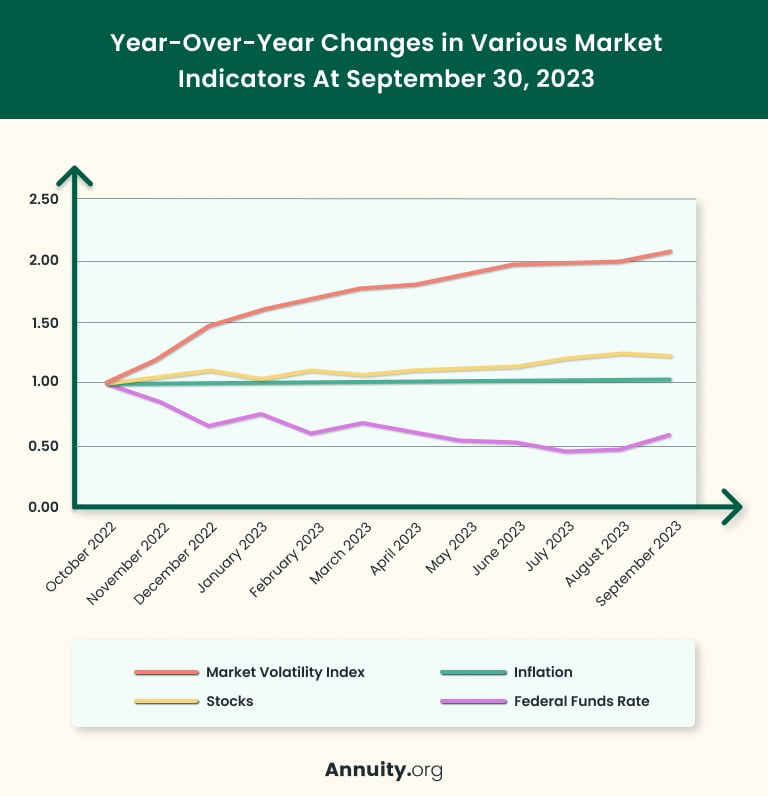

Despite this, stock prices have held up fairly well in the face of these obstacles. The chart below illustrates the relative change in short-term interest rates, inflation, stocks and volatility.

Source: Federal Reserve Bank of St. Louis, Economic Research Division

Risks Beyond Inflation, Interest Rates and Volatility

Although indexed annuities can mitigate investment risks related to inflation, rising interest rates or market volatility, they still carry inherent risk. The safety of these annuities ultimately depends on the financial stability and reliability of the insurance company that issues them.

To minimize particular risks, investors should conduct research on annuity providers. The Securities and Exchange Commission can be a valuable resource, as it acknowledges several credit rating agencies that assess insurance companies.

Annuities are investments, and as such, the principles of asset allocation and investment diversification apply to them as aptly as they do to buying stocks and bonds.

Investors should also assess the potential benefits of indexed annuities in alignment with their individual objectives and risk tolerances while thoroughly comprehending all associated risks.

While indexed annuities are affected by factors like Inflation, rising interest rates and market volatility, the protections they offer may make them appropriate for some investors.