With countless investment options to choose from, it can be challenging to weigh one investment against the rest. Luckily, metrics are available to help you evaluate your options while strengthening your financial literacy.

ROI is a measure widely used for comparing investment opportunities and their ability to generate economic value. Based on your financial goals, you can use ROI to make well-informed decisions for your retirement savings portfolio

What Does ROI Tell an Investor?

ROI tells investors how profitable an investment is. By calculating the ROI, an investor can determine whether an investment is worthwhile.

Thomas Brock, CFA charterholder and assistant vice president at a super-regional insurance carrier, told Annuity.org, “ROI is probably the most widely referenced investment metric in the finance world.”

ROI can apply to equity securities, fixed income instruments, commercial real estate and other business endeavors. It also evaluates the merit of investments in personnel, equipment and other business projects.

For example, if a shoe company pays $500 to host a booth at a running expo, and it earns $800 in sales as a direct result, this effort would have a positive ROI.

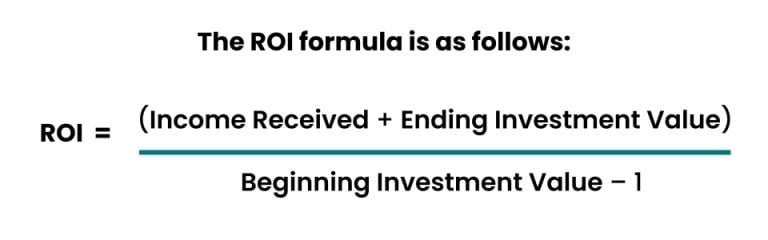

How Do You Calculate Return on Investment?

To calculate ROI:

- Add income received, including interest or dividends, to the ending investment value.

- Divide this number by the beginning investment value, including any start-up costs, like commissions or property taxes.

- Subtract one from that amount.

ROI Example

You invest $3,000 into a stock. After one year, you sell your shares for $3,900. You have $0 in dividends.

$0 dividends + $3,900 ending investment value = $3,900

$3,900 ÷ $3,000 original investment = 1.3

1.3 – 1 = 0.3, or 30% ROI

In this example, the 30 percent ROI measures the performance over a one-year span.

However, ROI can be misleading for longer-term investments because it does not specify the time necessary to earn the return on the investment.

Limitations of ROI

The standard ROI calculation does not reflect considerations for time value of money.

“This formula is ideal for computing the holding period return for an investment or the return for a discrete period of time — such as a quarter or a year,” said Brock, who is also a certified public accountant. “However, when assessing a long, multi-year investment, ROI can be deceptive.”

Time value of money refers to the concept that money is more valuable now than in the future, given that it can earn interest over time. Dollars invested today will have more time to earn compounding interest than dollars invested next year.

For example, a 200 percent return may appear to be a winning investment. However, if the investment earned this ROI over 30 years, 200 percent growth is far less impressive.

From one year to the next, the investment would have compounded at a significantly lower rate of return.

This formula will help you find the compound annual growth rate (CAGR).

How to Calculate Compound Annual Growth Rate (CAGR) CAGR = (1 + Cumulative Return) ^ (1 / Years) – 1 CAGR = (1 + 2.00) ^ (1 / 30) – 1 = .0373 |

In this case, the annualized return is only 3.73 percent.

Another way to gauge the performance of a long-held asset is to compute the internal rate of return (IRR). Like the CAGR computation, IRR factors in the time value of money and presents an annualized rate.

Return on Investment and Annuities

An investor can use ROI to compare the profitability of some, but not all, annuities.

“If the basic terms of an annuity — amount of upfront investment, amount and frequency of future income payments and duration of the income payments — are known with certainty, it is not difficult to calculate an ROI for an annuity,” Brock said.

However, depending on the type of annuity, unknown and unpredictable factors can make it virtually impossible to determine the ROI.

Annuities that guarantee income for life include an unknown factor: the exact date of the annuitant’s death. With lifetime income annuities, payments stop upon the annuitant’s death, so the actual ROI is not fully realized until the annuitant dies and the contract ends.

“Just like with life insurance, lifetime income annuities have the potential of providing the best return on investment that you will never see,” MarketWatch explains.

Instead of using ROI, the insurance company will quote lifetime annuity payouts in a clearer, more accurate calculation — in terms of cash flow, or the cash the annuity will generate.