Source: U.S. Bureau of Labor Statistics

Source: U.S. Bureau of Labor Statistics

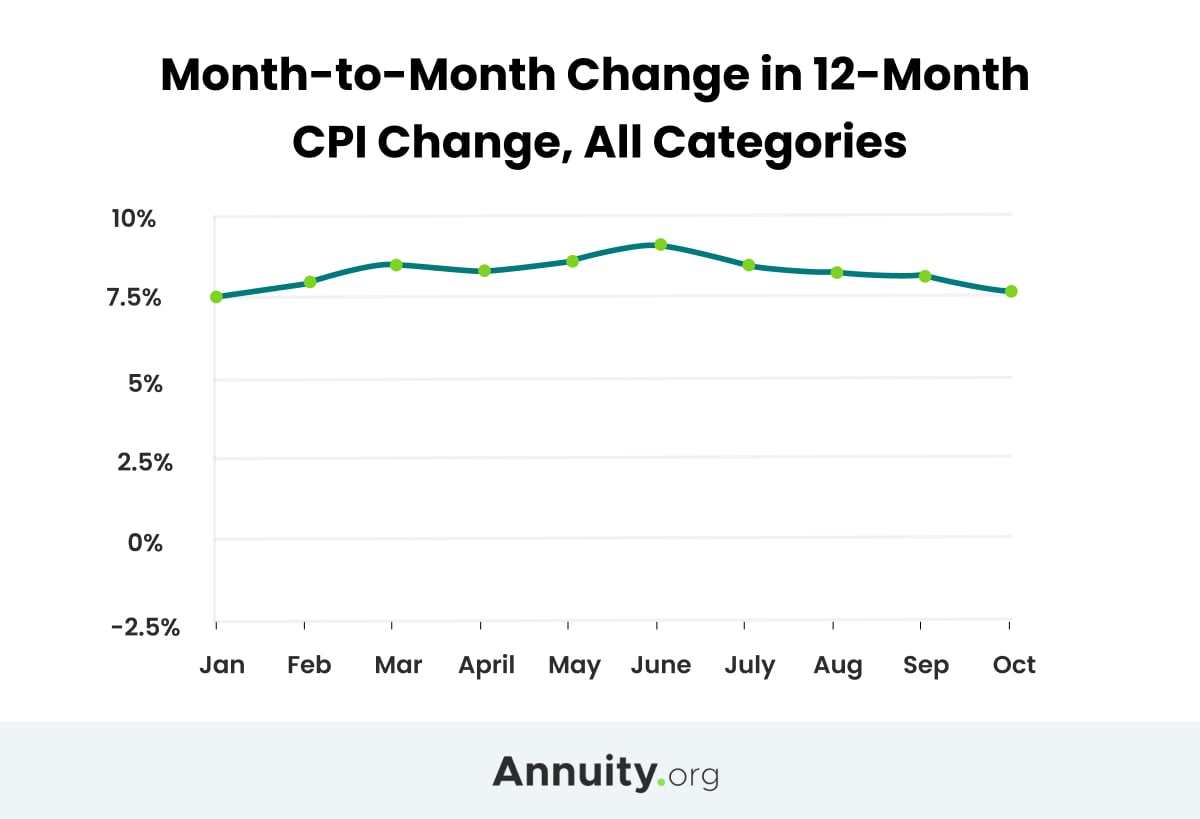

The Federal Reserve has rolled out a steady stream of interest rate hikes over the past year to slow climbing inflation. It’s expected to slow the hikes going into 2023, but the rates remain the highest in years, according to an article by Reuters.