Home / News / 6 Tips To Build a Conservative Investment Portfolio

6 Tips To Build a Conservative Investment Portfolio

Over the past decade or so, investors have experienced historically low levels of volatility. This is largely due to the unprecedented fiscal intervention employed by the Federal Reserve in the wake of the Great Recession. Essentially, the Fed flooded capital markets with immense amounts of liquidity and kept the federal funds rate near zero for about 10 years.

The resulting environment — which was widely viewed as unsustainable — was superb for borrowers and stock investors, but extremely challenging for savers and fixed-income investors. The Fed launched a short-lived campaign to normalize rates in 2017, but the COVID-19 pandemic prompted it to retrace its steps, taking its benchmark rate back to zero where it remained for nearly two years.

Now faced with soaring inflation, the Fed has aggressively raised the federal funds rate to 3% and appears poised to take it even higher. This dramatic increase has had a pronounced ripple effect on loans of all types and tenures. It has also fueled elevated levels of stock market volatility and stoked widespread economic uncertainty, both of which have been exacerbated by the war in Ukraine.

All of this is incredibly nerve-racking for investors, which brings us to the purpose of this post — to highlight six tips you can use to build a conservative investment portfolio.

1. Establish a Cash Reserve

Investing is a smart way to build wealth. However, you need to establish an adequate cash reserve before you put your money into assets exposed to price fluctuations, potential loss of capital and liquidity lockups.

If you’ve established a sound budget, eliminated any problematic debt (such as credit cards and personal loans) and funded an emergency reserve amounting to at least six months of expenses, it’s time to focus on investing and harnessing the power of compound interest. The sooner you can do so, the better for your bottom line.

Pro Tip

I believe that the best place to put your cash reserve is in a high-yield savings account. The most competitive institutions are currently offering 2.00% to 3.00% interest.

2. Determine Your Investing Time Horizon

The foundation of any investment portfolio is an estimate of your time horizon, the time until you expect to draw down on your principal investment and accumulated earnings. The longer the time horizon, the greater your growth potential and the more risk you can comfortably assume. Conversely, the shorter the time horizon, the lesser your growth potential and the less risk you can comfortably assume.

Fast Fact

Generally, a time horizon of 10 years or less is considered short while a time horizon of over 10 years is considered long.

3. Familiarize Yourself With Key Asset Classes

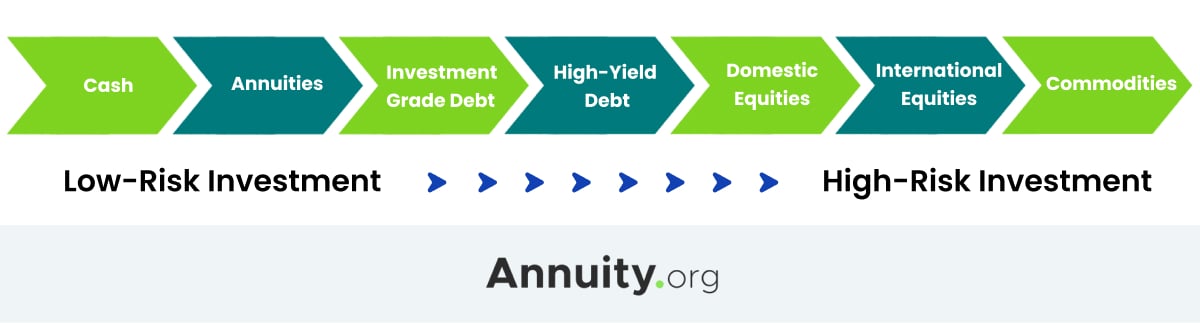

The asset classes available to most investors include publicly traded equities, publicly traded debt instruments, commodities, annuities and cash. We generally define the riskiness of these assets in terms of the price volatility they exhibit. By this standard, I’ve illustrated a breakdown from some of the least risky asset classes to the riskiest below.

The assets toward the leftmost end of the diagram are the most appropriate for conservative investors. They emphasize capital preservation and income generation over focusing on growth.

It’s best to ensure that you wholly understand anything you put your money into. This calls for some basic research into these readily accessible asset classes or, ideally, leveraging the assistance of a trusted financial advisor. If you want help but are cost-conscious, you can tap a knowledgeable family member or find a robo-advisor.

4. Establish a Prudent Asset Allocation Strategy

Once you’ve sized up your investing horizon and familiarized yourself with appropriate asset classes, it’s time to formulate an asset allocation strategy. It needs to reflect high liquidity and it should provide you stability and a high degree of income. Your cash reserve accomplishes the first objective; A healthy allocation to investment-grade bonds can achieve the second and third objectives.

That said, don’t overlook the importance of incorporating a growth component into your portfolio. The most conservative way to do so is via large-cap, defensive stocks, particularly those in the utilities and consumer staples sectors. These stocks exhibit resiliency during economic downturns, and they kick off dependable dividends.

5. Leverage Efficient Investment Vehicles

Buying individual investments isn’t an efficient way to build a conservative investment portfolio. It’s overly expensive, time-consuming and unlikely to yield an optimal degree of diversification. Utilizing low-cost, fund-style investment vehicles such as exchange-traded funds (ETFs) and mutual funds is a much better approach.

Both of these vehicles can provide highly diversified access to an asset or group of assets, and both are sponsored by some of the largest, most reputable investment companies in the world. ETFs trade, like stocks, are bought and sold throughout the day at fluctuating market prices, while transactions of open-ended mutual funds are completed directly with the fund company at prices determined at the end of each trading day based on the fund’s underlying assets.

Mutual funds can be actively or passively managed. Most ETFs are relatively low cost and passively managed, tracking well-known indices such as the S&P 500 and the Nasdaq Composite.

6. Rebalance Your Portfolio

Be diligent about monitoring your portfolio and periodically rebalancing your investments back to your strategic asset allocation. Assuming no influxes of cash, this means selling some of the outperforming assets and buying more of the underperforming assets.

If you work with a robo-advisor or a full-service financial advisor, there is no need to do any rebalancing. This task is part of their service offering and will be completed automatically based on the terms established at the onset of your relationship.

Please seek the advice of a qualified professional before making financial decisions.

Annuity.org doesn’t believe in selling customer information. However, as required by the new California Consumer Privacy Act (CCPA), you may record your preference to view or remove your personal information by completing the form below.

Your web browser is no longer supported by Microsoft. Update your browser for more security, speed, and compatibility.

If you are interested in learning more about buying or selling annuities, call us at 866-924-8052

The assets toward the leftmost end of the diagram are the most appropriate for conservative investors. They emphasize capital preservation and income generation over focusing on growth.

It’s best to ensure that you wholly understand anything you put your money into. This calls for some basic research into these readily accessible asset classes or, ideally, leveraging the assistance of a trusted financial advisor. If you want help but are cost-conscious, you can tap a knowledgeable family member or find a robo-advisor.

The assets toward the leftmost end of the diagram are the most appropriate for conservative investors. They emphasize capital preservation and income generation over focusing on growth.

It’s best to ensure that you wholly understand anything you put your money into. This calls for some basic research into these readily accessible asset classes or, ideally, leveraging the assistance of a trusted financial advisor. If you want help but are cost-conscious, you can tap a knowledgeable family member or find a robo-advisor.