How an IRA Can Be Used to Purchase an Annuity

An IRA already provides tax-deferred growth, making it a common vehicle for retirement savings. Using part of an IRA to purchase an annuity doesn’t add new tax benefits, but it can change how and when your money is used in retirement.

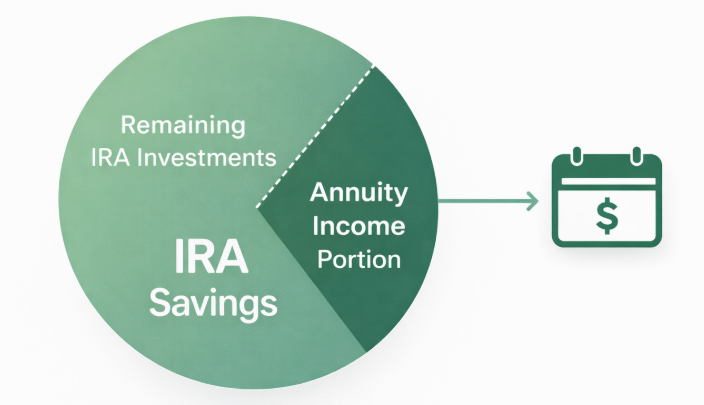

Instead of relying solely on market-based withdrawals, some retirees choose to allocate a portion of their IRA to an annuity designed to provide steady, predictable income, often for life. Depending on the structure, income can begin right away or at a future date.

When IRA funds are used to purchase a qualified annuity, the money typically remains tax-deferred, and payments are taxed as ordinary income when received—similar to other IRA withdrawals. Many retirees use only part of their IRA, allowing them to balance guaranteed income with ongoing investment flexibility.

Two Common Ways to Use IRA Funds

The way IRA funds are used to purchase an annuity matters just as much as the product itself. Understanding these two approaches can help you avoid unnecessary taxes and make a more informed decision.

| Option | Best for | What happens | Biggest “watch out” |

|---|---|---|---|

| Direct IRA transfer (recommended) | Most retirees | IRA custodian sends funds directly to annuity provider | Must remain within qualified accounts |

| Distribution then purchase | Limited cases | You withdraw IRA funds, then buy an annuity | Triggers immediate taxation |

Our Three-Step Process

Understand Your IRA

We review your age, IRA type, and whether income, stability, or legacy planning is the priority.

Compare Annuity Structures

Fixed, indexed, immediate, or deferred—each works differently and will depend on needs.

Review Income Scenarios

If appropriate, you’ll see estimated income ranges and trade-offs before deciding.

Annuity.org: A Resource You Can Rely On

We help retirement savers understand IRA rules, compare annuity structures, and avoid costly mistakes—so you can decide with confidence. Our approach focuses on education, clarity, and helping you understand your options before making any decisions.

What Our Readers Say

-

“He was there for us every step of the way. He was responsive, patient, and considerate of all our needs. We live in Oregon, and, quite frankly, John was more responsive to our needs than anyone we could find in the Portland metro area. I feel very comfortable in recommending him and his firm. They are knowledgeable and very qualified at what they do!!!”Richard J.

“He was there for us every step of the way. He was responsive, patient, and considerate of all our needs. We live in Oregon, and, quite frankly, John was more responsive to our needs than anyone we could find in the Portland metro area. I feel very comfortable in recommending him and his firm. They are knowledgeable and very qualified at what they do!!!”Richard J. -

“Found Annuity.org to be a wealth of information that helped my wife and I decide a) whether an annuity should be part of our investments portfolio and b) locating the best-rated annuity providers and finding a local representative.”Ron Thompson