How a 401(k)-to-Annuity Rollover Works

Rolling over an old 401(k) can be a smart move when you leave a job or start planning for retirement—but how you do it matters just as much as where the money goes.

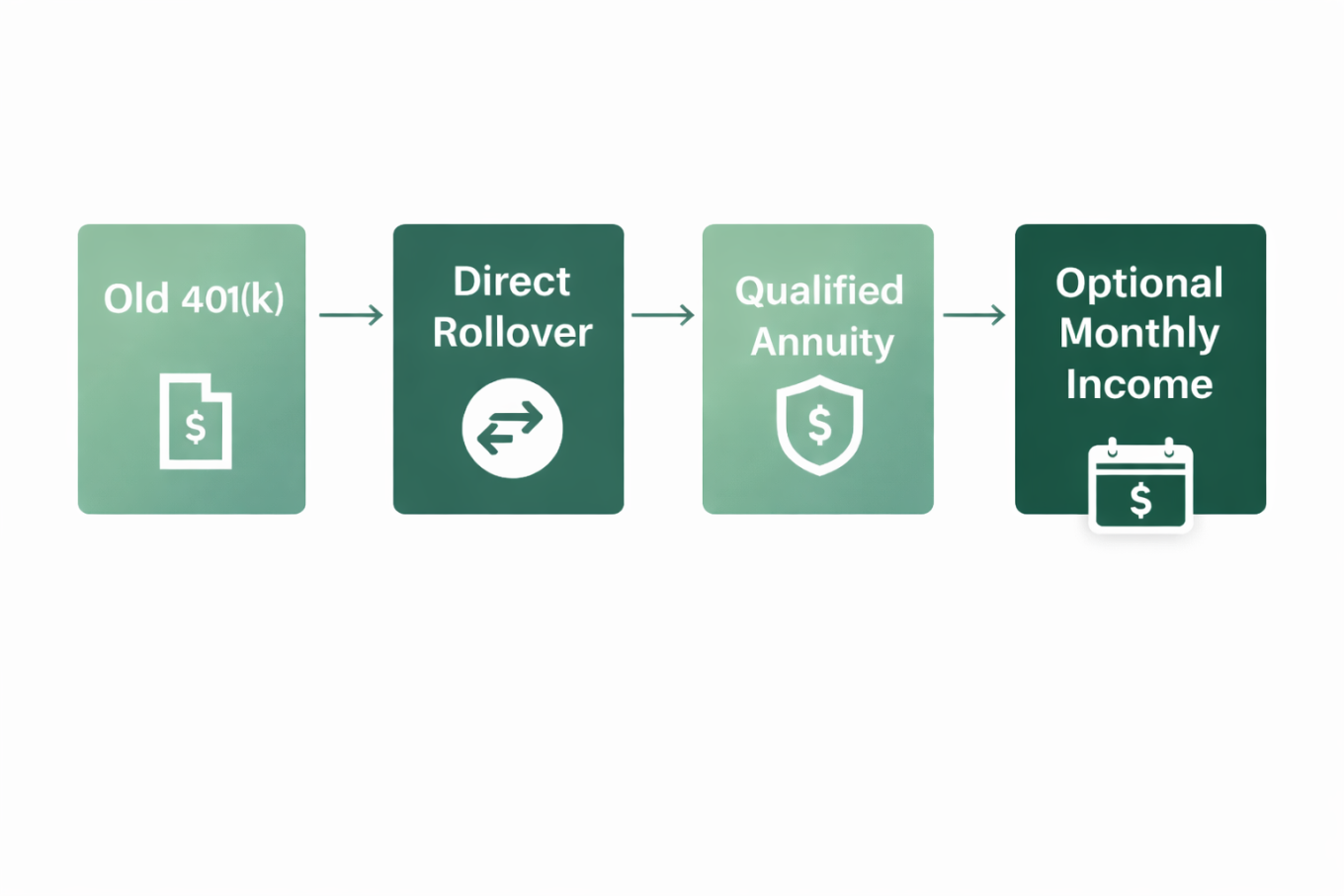

Many retirees explore annuities as part of a rollover strategy because they’re designed to help turn retirement savings into predictable income, rather than long-term accumulation. When handled correctly, a 401(k) rollover into a qualified annuity can remain tax-deferred and give you options for income you can’t outlive.

That said, not all rollovers work the same way. Certain methods are straightforward and commonly recommended, while others come with strict deadlines, withholding rules, and potential tax consequences if even one step is missed.

Two Ways to Roll Over

Before you move any money, it’s important to understand how a 401(k) rollover actually works. Most retirees choose one of the two methods below—each with very different tax and timing rules.

| Option | Best for | What happens | Biggest “watch out” |

|---|---|---|---|

| Direct rollover (recommended) | Most retirees | Funds transfer from custodian to the annuity provider | Make sure the check is payable to the new custodian—not you |

| Indirect rollover | Rare cases | You receive funds, then redeposit into the annuity | Withholding + 60-day deadline can trigger taxes/penalties if missed |

Our Three-Step Process

Tell Us What You Have

Share your approximate 401(k) balance, age range, and goals (income, safety, legacy).

Get a Free Rollover Review

A specialist walks you through direct rollover steps and product types (fixed, indexed, deferred/immediate).

Choose the Income Approach

If it’s a fit, you’ll see estimated income ranges and trade-offs—then decide what to do next.

A Resource You Can Rely On

We help retirement savers understand rollover rules, compare annuity structures, and avoid costly mistakes—so you can decide with confidence. Our approach focuses on education first, clear explanations, and no-pressure guidance as you explore your retirement income options.

What Our Readers Say

-

“He was there for us every step of the way. He was responsive, patient, and considerate of all our needs. We live in Oregon, and, quite frankly, John was more responsive to our needs than anyone we could find in the Portland metro area. I feel very comfortable in recommending him and his firm. They are knowledgeable and very qualified at what they do!!!”Richard J.

“He was there for us every step of the way. He was responsive, patient, and considerate of all our needs. We live in Oregon, and, quite frankly, John was more responsive to our needs than anyone we could find in the Portland metro area. I feel very comfortable in recommending him and his firm. They are knowledgeable and very qualified at what they do!!!”Richard J. -

“Found Annuity.org to be a wealth of information that helped my wife and I decide a) whether an annuity should be part of our investments portfolio and b) locating the best-rated annuity providers and finding a local representative.”Ron Thompson